I have yet to make the kind of post I intended to make when I started the blog but as I was brain storming today and trying to think about pertinent concepts to blog about I thought of another subject that has been completely ignored by the mainstream media. The average American has now spent hours reading or listening to news about the financial crisis. The "news" on CNBC and other nightly news programs talk constantly about the current crisis but never actually explain in detail what any of the stuff they are talking about is. Now I consider myself pretty knowledgeable in the realm of finance but I must admit I spent several months reading about CDO, CMOs, CLOs and the CDS before I finally got frustrated and decided to go on a mission to understand what all of this junk was (turns out it actually was all junk). Journalist were content to just read what was on their prompter or quote other "financial guru's" but not actually understand what they were writing about. We were bombarded with these acronyms but no one has ever explained why they are a problem. Sounds a lot like what got us in this mess in the first place. I spent the better part of a month researching and reading about these different products to understand what it was exactly these financial instruments are and why they are so dangerous. So here goes my attempt to compile my findings in a format that can hopefully be understood by everyone. If you have no interest in understanding some of the more complex financial instruments behind sub-prime lending then you should probably skip this post completely.

Here is a quick and easy guide to what the acronyms stand for:

CMO = Collateralized Mortgage Obligation

CLO = Collateralized Loan Obligation

CDO= Collateralized Debt Obligation

CDS = Credit Default Swap

Great! Now we are getting somewhere. Much farther than most articles would ever take you. I don't know about you but I was always taught to write out the phrase the first time I used an acronym; apparently this lesson was lost on our media.

To really understand what all of these "new" financial instruments actually are, it's probably easiest to start with a high level look at how the financing arm of a bank may operate. Remember I'm keeping it as simple as possible here, there are many intricacies and nuances not covered in this article.

Suppose for a second that you are a bank that has 100 companies you lend to. All of these companies are paying 1 million in interest per year and have credit ratings of BBB. You estimate that 1 out of every 10 of these companies will default on their obligations but have no way of knowing which 10 it will be. You currently have a book of 100 loans, paying a an estimated 90 million a year in interest. This is how many banks operated for a very long time.

Now things start getting interesting. Instead of holding the 100 loans you decide to sell off the rights to the interest payments by creating a security that has rights to the stream of payments these loans generate but instead of selling this as one big chuck you divide it up into sections called tranches. Pay close attention here, this is important. The way you divide this is by creating several different packets (tranches). Remember we estimated that 1 in 10 of these companies will default, so at any given time we could reasonably expect at least 90 million in interest to be coming in. So the first section we create is the rights to the first 85 million in interest paid. What this means is, when the companies make interest payments no matter which companies are making payments, the first 85 million goes to the owners of this first tranche. Since we expect at least 90% of the companies to stay current on their loans when we issue this security it gets a AAA rating because there is virtually "no chance" that more than 1 in 10 of these companies will default on their loan, but wait I thought all the companies had a BBB rating (indicating they are slightly unstable and may not make good on their payments in bad economic conditions)? Ohh well just ignore that for now.

The economy is on fire and these companies are doing so well, no one is defaulting so we can sell off the second packet (tranche) which is the right to the next 5 million in interest payments which is also considered pretty solid since we only expect 1 in 10 to default. This packet gets a rating of A.

There is the leftover rights to the 10 million which based on our own model we would assume is worthless since we do not predict more than 90 of the companies to be current. Still since the economy is doing so well there is someone out there willing to bet only 8 instead of 10 we predict will default so we can sell this last package for pennies on the dollar to a speculator. We package the rights to any remaining payments and sell it as junk and allow very risk tolerant investors to speculate on the fact less than 10% of the companies default. This idea in and of itself is good for the economy. It allows banks and risk adverse investors to pass on the risk of owning these assets to someone who is willing to take the risk. The problem comes when the person who buys this "junk" values it much higher than it's really worth because in favorable economic conditions more companies are making good on their loans and the holders of these assets being to assume that this is the norm.

So now we have a bank with 100 million in interest coming in per year.

The first 85 Million goes to Tranche A (AAA) rating

The next 5 million goes to Tranche B (A) rating

The leftover 10 million Tranche C (C) is speculative but could potentially payoff big.

The bank now sells Tranche B and C to hedge funds, pension funds, and whoever else is stupid enough to buy it. Since banks are risk adverse they will even sell off a portion of the A tranche to limit their risk only to the first 60 million in payments. Now since the default rate was estimated at 1 in 10 and the banks have sold off and hedged themselves against roughly 40% of the payments. The first 60 million in payments is believed to be essentially riskless since there is no way 40% of the companies could stop payment at one time. Our genius has created what was known as a super senior tranche of income made up of BBB company debt. Who cares if the whole portfolio is made up of BBB rated companies, we essentially made an entire portfolio that is rated AAA instead of BBB. Remember the saying there is no such thing as a free lunch? Well apparently that doesn't apply to super smart bankers. Now they have their cake and can eat it too. There is no need to hedge the remaining 60 million because it is so super safe the banks can just collect interest and consider it a riskless position, they effectively isolated all their risk and sold it off....or so they thought.

Going through this kind of securitization is a huge plus for the banks since they don't have to worry about these assets they are holding ever going bad (or so they thought). They considered these riskless investments and did not insure themselves against them and were not required to hold much capital to compensate for any losses. This means they can make even more loans. Since everyone likes money and everyone wants more of it, especially those greedy shareholders, why stop with packaging up corporate debt. Banks observed similar tendencies in mortgages. Sure if we make $300,000 sub prime loans to unqualified people that can't even qualify for a car loan; some of them will default but only SOME of them will. Essentially follow the same process as above but with mortgages instead. We loan 1,000 people money to buy a house, and we know these are all sub-prime borrowers so the chances we get paid back may only be 70% but that's ok we sell off that 30% risk by bundling these loans and selling the 30% to someone willing to take on the risk. This was also a very profitable process because the banks made money every time they packaged these loans. They would make a markup on the difference between the intrinsic value of the individual mortgages and the eventual sale price of the combined tranches; plus whoever was managing the mortgages got an ongoing management fee.

Now it where it really gets tricky and this next idea is true genius. Suppose we do this process 10 times. So now we've taken 10 packages of 1,000 mortgages and split them up into tranches as we did with the corporate debt in the example above. Based on our models the first 70% seems fairly safe and secure so we don't really have much problem selling that portion off or keeping it on our books but that last 30% is harder to pass off individually. People can look at our models and estimate using their own models and come to the conclusion that the lower rated tranches are pretty worthless. Some may assume they can make a profit because their model only predicts 25% will default and we could possibly sell it for more than we would assume it's worth, but it's a hard sell. So instead of trying to sell this "leftover" tranche all alone we re-securitize the leftovers into one super mangled mess of junk called a CDO. Essentially we start the process all over again with that last 30%. Take all 10 of the leftover tranches put the rights to any remaining payments together and then split them up into A, B, C, D etc. tranches. So that if any of our MBS (Mortgage backed securities) have any leftover payments above our estimated 70% it will flow into the A tranche of the CDO. Once the A tranche is paid, any remaining leftovers will flow to the B tranche and so on. It looks something like this.

10 individual MBS each generating 100 Million in interest

A tranche first 50 million

B tranche next 20 million

C tranche next 10 million

D tranche (junk) last 30 million (if paid)

Now you do this 10 times and take all of the leftover D tranches with rights to any of the remaining 30 million and repackage them.

10 D tranches with rights to any of the remaining 300 million

A tranche has rights to the first 20% of remaining payments

B next 20%

C next 20%

D last 40%.

What is amazing is the A tranche of these CDOs were getting AAA ratings because people were making good on their mortgages and that stream of income was considered guaranteed. There was even some left over for the B, C, and D folks. Now lets see how this can blowup fast. Suppose we are in a world where currently 82% of these sub-prime mortgages are paying interest. That means everyone in tranche A,B, and C is getting paid from the original securitization and everyone in tranche A and B of the CDO are getting paid, nothing left for C, D except possibly some hope of recovery if the foreclosures sells for more than the notational value of the mortgage. That's ok though, no on expected them to pay anyway and they sold for mere pennies on the dollar. Well what happens if the default rate on sub prime mortgages drops just 3%. The income stream being generated by Tranche B is cut in half. If it drops another 3% tranche B is now worthless, if it drops to 70% (which is what we originally predicted) now the entire CDO is completely worthless because there are no leftover payments. So one day you hold an asset generating 120 million in interest per year, the next day it's generating nothing. For a graphical representation of this concept checkout this great

illustration. Merrill Lynch was the first to try to sell one of these super senior CDOs (meaning the A tranche of a CDO). It's notational value was 30.4 billion and they sold it for 6.7 billion, 75% of that 6.7 billion was actually a loan to the purchaser...from none other than...Merrill Lynch. So they basically loaned Lone Star Funds (the purchaser) the money to buy an asset they had initially valued at 30.6 billion for only 6.7 billion. Talk about a great business move. Based on this logic one garbage bag may be worthless but if you take a whole bunch of garbage bags together (also known as a dumpster) somehow it is worth something.

Now we have just one more issue to address. Suppose you were a buyer of one of these CDOs that happens to be paying well right now but you are smart and you know that times could change and you want to protect yourself if it does default. This is known as a Credit Default Swap and it is an insurance contract you can take out against a bond defaulting. So now you have bought protection on your holdings and hopefully if you do it right the premium for the insurance is lower than the interest you receive by holding onto that bad debt. But what happens if the person who you bought insurance from is accepting premiums by insuring trillions of dollars of the same garbage debt and there is no way they could possibly ever of have the liquidity if their bets went against them? This is like buying insurance on a house on the coast of Florida after a hurricane has already been spotted on the Doppler radar. Not only that but you and everyone in else in your neighborhood bought insurance from the same company. Joe Schmoe insurance (read: AIG) figures they are smarter than the weather people who predict the hurricane will hit Florida and their weather man predicts it will spin harmlessly off into the mid-Atlantic. So Joe Schmoe takes the $500,000 collected from insurance premiums on your neighborhood and throws a huge party for him and his 10 best friends and declare himself the most profitable insurance company in the history of business. Yet you consider your house 100% safe even if the hurricane hits your insurance will payoff and you can get a new one. Opps the hurricane does hit and now Joe Smchoe owes 50 people $250,000 each and he already spent the origional $500,000 on a party and put the leftovers in a CDO that is now worthless!!! Lucky for you Uncle Sam (our taxpayer dollars) stepped in to guarantee a lot of this insurance that would have otherwise not been paid.

Up to this point all of our models have been based on known information and we would never expect more than 30% of these sub-prime mortgages to default at one time. What happens if the estimated 30% becomes 50% or those companies that were only defaulting on 1 in 10 loans start defaulting on 3 in 10. As the example above shows those lower tranches and even some of the less senior tranches of the original MBS become worthless. All this paper that we thought was super safe is now worth nothing and what's more no one will loan you the money you need to pay back the money you borrowed to buy CDOs! So now no one will loan anyone any money to pay any of their loans. See how this spirals out of control quickly? It is ok though you can rest peacefully at night knowing that more than 1 trillion of your children s tax dollars have already been spent and another 2 trillion has been pledge as a backstop against further losses for those lending to these financial giants and possibly another 800+billion is in the pipe to get this whole mess sorted out.

It is possible when times get better and if the government continues to redistribute our nation's wealth to those who irresponsibly borrowed more than they could afford, those who loaned more than they should, and those companies than spent years making billions writing insurance they couldn't honor these mortgages will stop defaulting and some of those less senior tranches will again be worth something. Only time will tell. Until then expect the numbers to get bigger than you could possibly imagine. We are already at the point where the numbers are so gigantic that no one can honestly picture how much money we have spent, loaned and borrowed to get out of this mess. So how much of our future tax dollars are we spending? 3 trillion could buy 104,748 tons of gold at at price of 900 an ounce. You ask how much is 104.748 thousand tons of gold? Twelve times as much gold as the U.S. has in their national reserves in Fort Knox and more than triple the worlds gold held in national reserves.

As I said in the beginning this is a VERY VERY Simplified version of what actually occurred but it can at least give you a taste of what was going on in these gigantic financial institutions. There are plenty of resources if you feel the desire to investigate this further. One of the blogs I link on the right

Calculated Risk had an amazing series of articles written by a blogger known as Tanta who wrote about the sup-prime mortgage crisis well before things started looking bad for the rest of us.

Feel free to comment on the post or send me an email with further questions. I will do my best to find the answer.

TRC

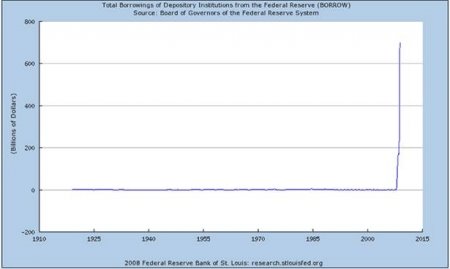

Hats off to East Coast Economics; they published these graphs. Original article can be found here. Thought this would be interesting to share to help put a little perspective on what we are going through. Remember the Federal reserve is suppose to be the "lender of last resort." Right now banks can get money from the fed for 0.00% interest and then deposit it back with the Fed and earn .25% interest.

Hats off to East Coast Economics; they published these graphs. Original article can be found here. Thought this would be interesting to share to help put a little perspective on what we are going through. Remember the Federal reserve is suppose to be the "lender of last resort." Right now banks can get money from the fed for 0.00% interest and then deposit it back with the Fed and earn .25% interest.